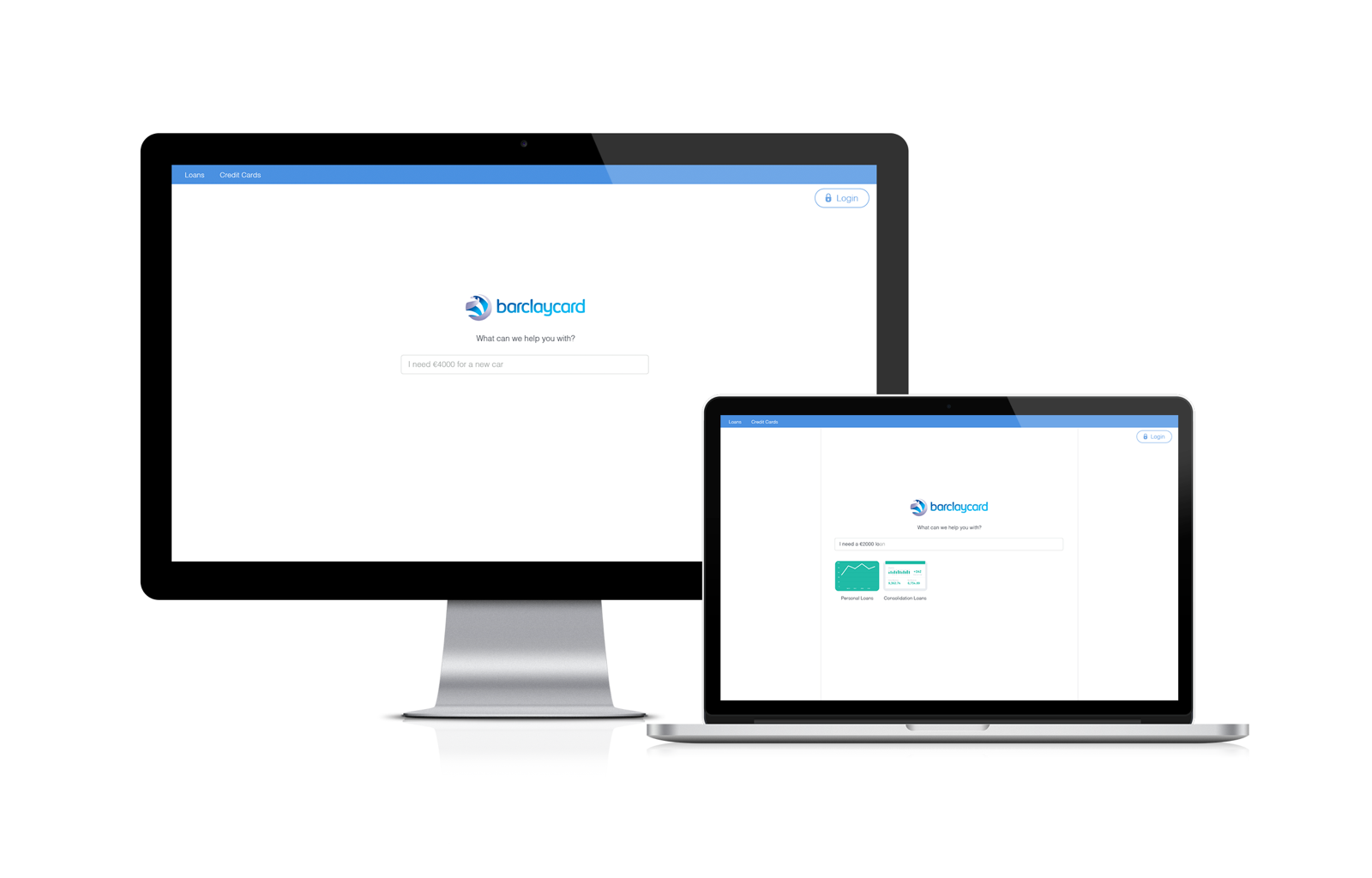

You need to borrow $2,000 to purchase a new fridge for your house. You’d like to find out more about what Barclaycard has to offer and complete your personal loan application online. This is the journey of European Consumer Lending.

BARCLAYCARD

Barclaycard

LONDONTOWN

I arrived in London to join a team that was creating a mobile website for a Barclaycard strategic growth opportunity in the consumer leading sector, specifically personal loans. My focus was to identify interactive features that would validate customer needs, create user journeys and personas for the customer proposition, design a prototype to simulate the customer journey and test the propositions and prototypes with potential customers.

VISION

Market and customer research had been driving this initiative for Barclaycard Germany. These insights defined the product’s vision to build a digital service which enables customers to interact with Barclaycard in a personal way, on any channel they wish with intelligent and interactive content to connect customers with the details that matter to them, when they matter to them.

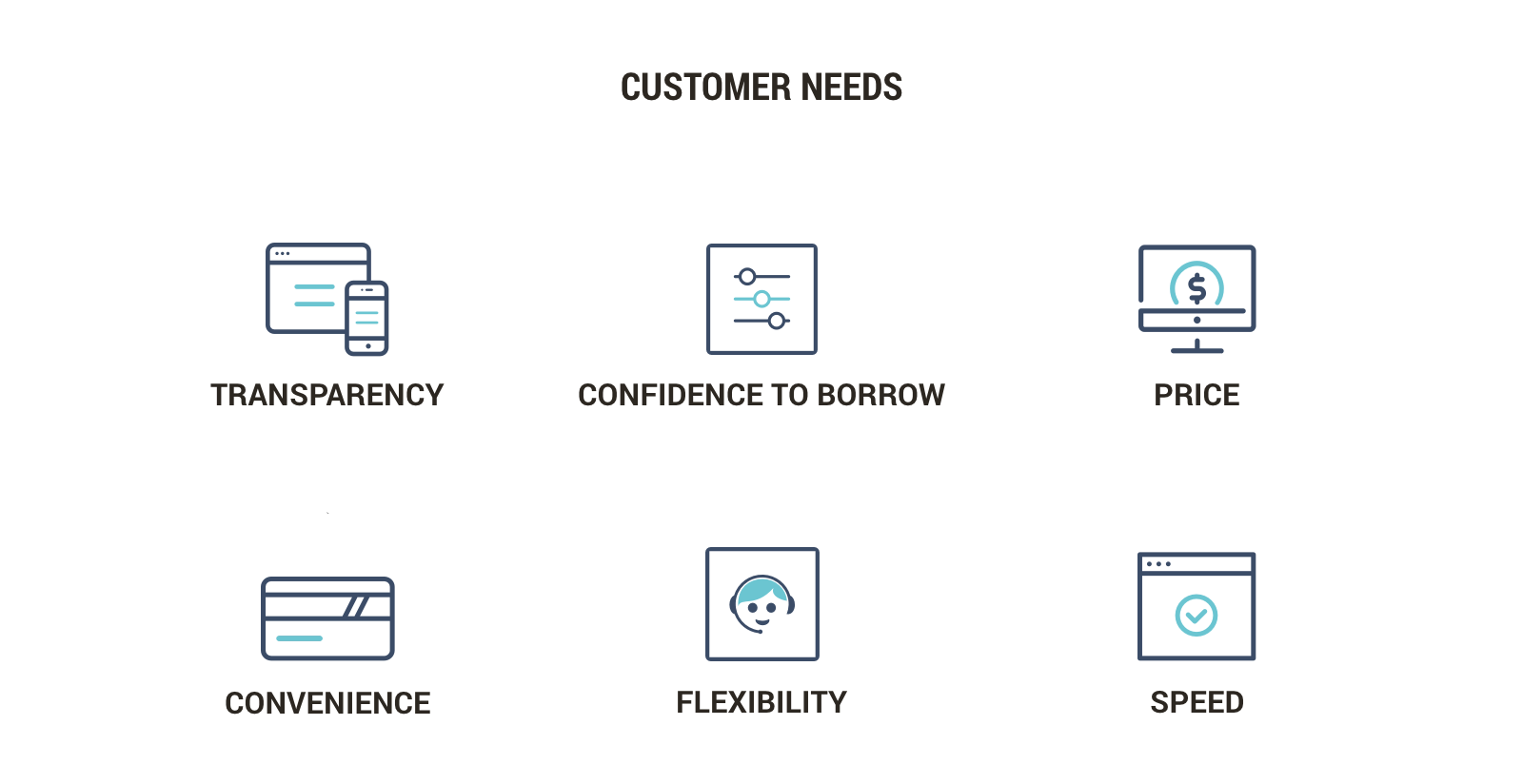

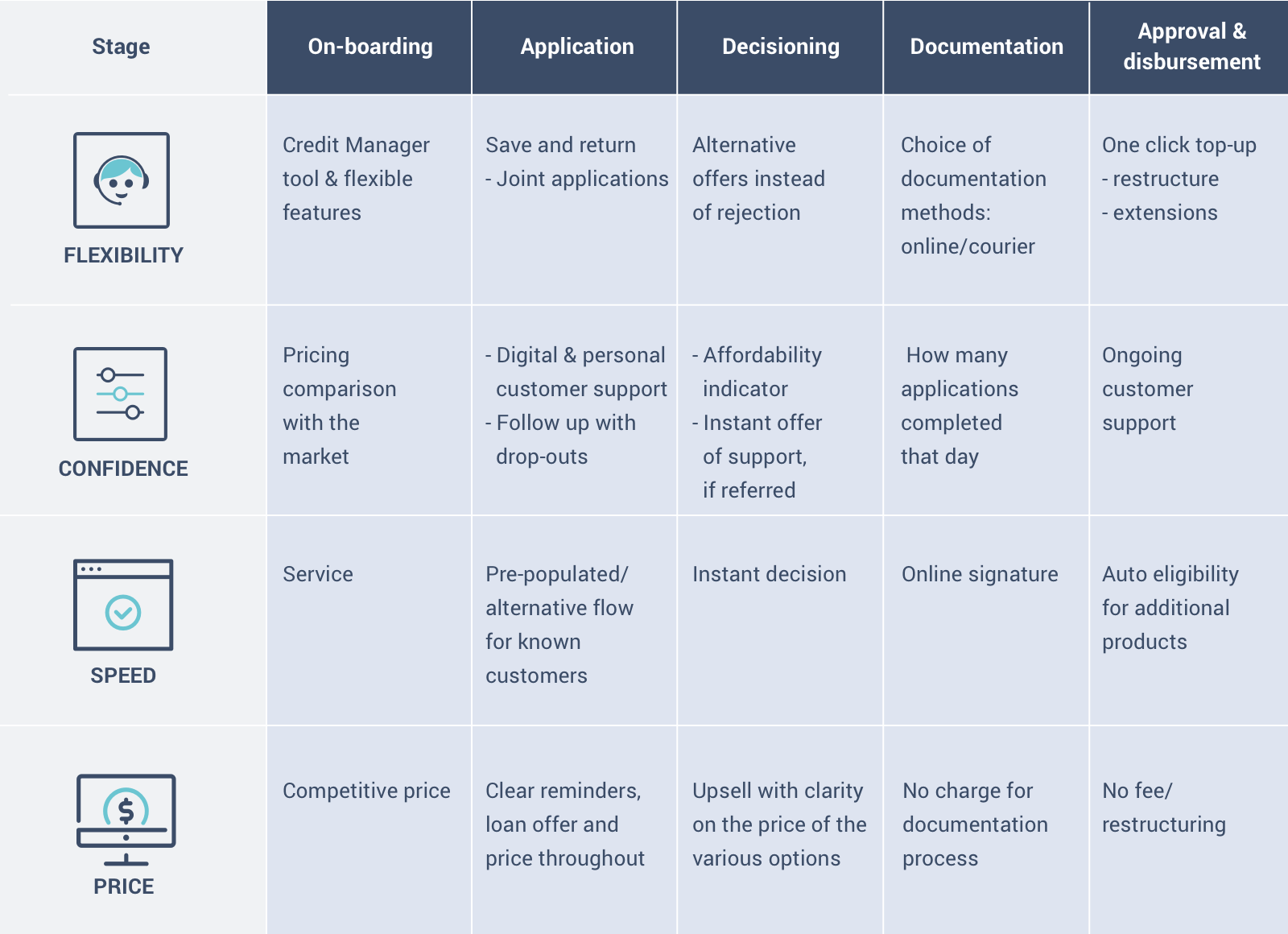

CONSUMER INSIGHT

Our customers highlighted key factors that they take into consideration when taking out a loan: – A monthly repayment amount within the family budget – Fixed or variable interest rate – The duration of the loan – Flexibility to alter repayments and rely on insurance if circumstances change – Credibility of lender and strength of their reputation – Transparency of loan terms and whether there are any additional fees – Easy application process – Fast approval and payment

“I need to know I can afford the loan and it is a good price. It should be quick and easy to apply for and flexible in case my circumstances change. When I apply, I need jargon free expert support from a place I can trust with no hidden costs.”

- Barclaycard consumer

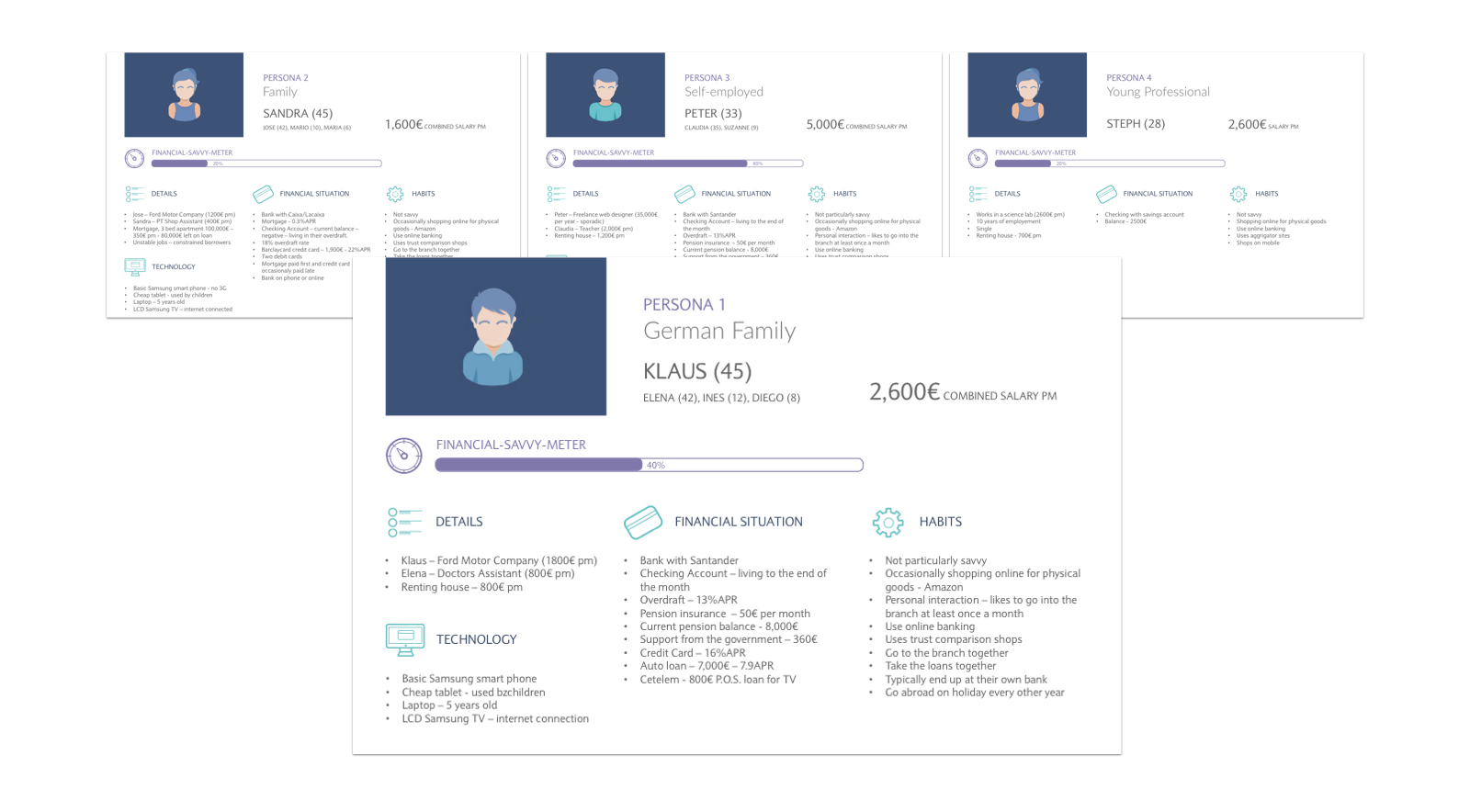

PERSONAS & USER JOURNEY

From our research we created four personas which we used when analyzing our customers’ needs to define their diverse context of use.

CUSTOMER JOURNEY

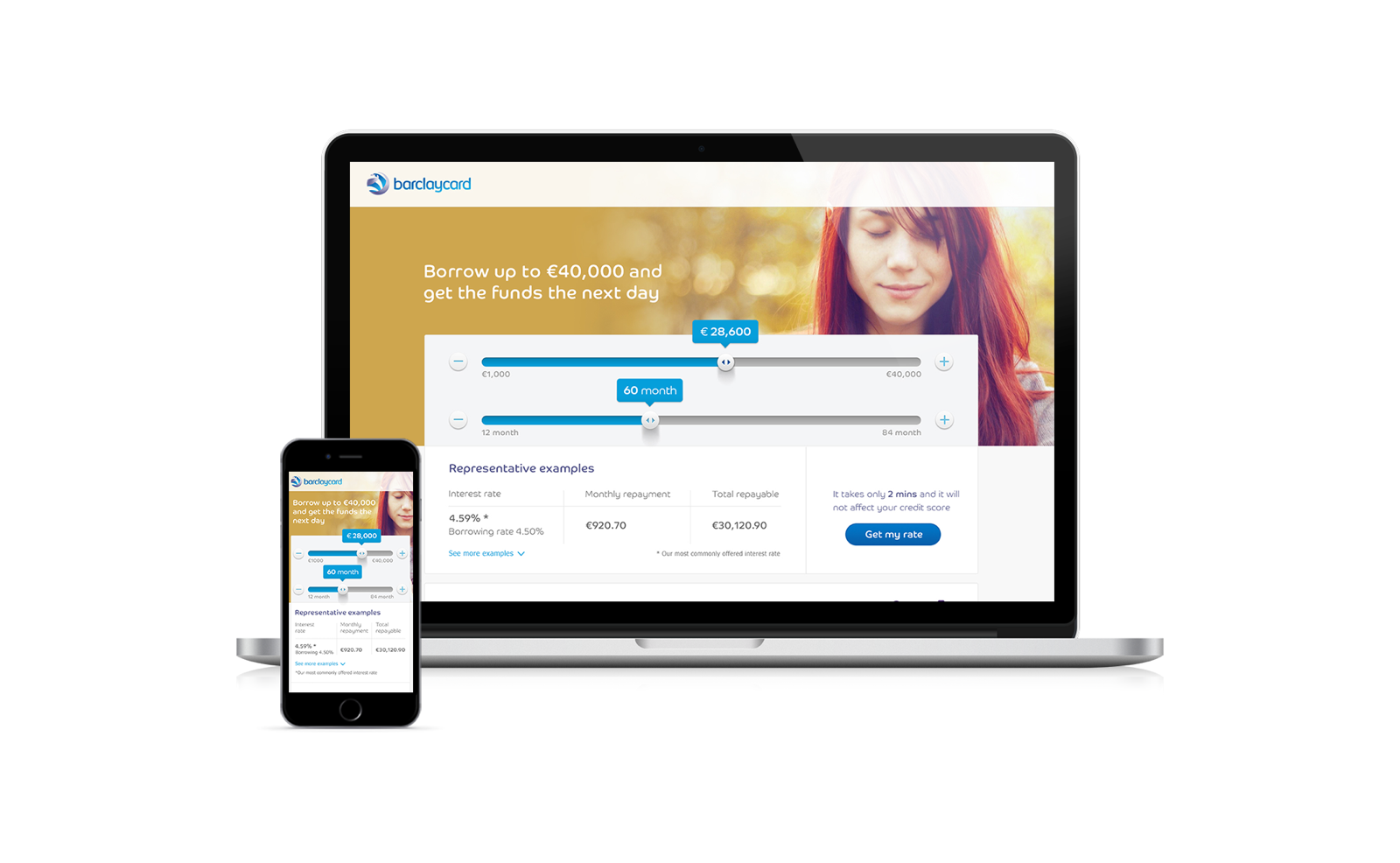

Customer arrives on the website, begins searching for loan products, compares the costs of loans and additional features.

DIGITAL JOURNEY

We created a high level look at how this translates into a digital experience. The traditional digital experience consist of a series of web pages, sometimes the experience can include a live chat with customer support. These interactions and experiences are disconnected and the outcome is not transparent, conversations are lost and this does not give users a sense of control. Based on user research the proposal was to bring the feedback of the consumer into a real-time relationship stream. A transparent experience where all communication is saved, organized and presented in a clear and relevant way. Communication can be delivered by an in-depth knowledge base that recognizes human language or by a Barclaycard agent so that communication extends beyond chat. It includes statements, letters, emails and phone calls.

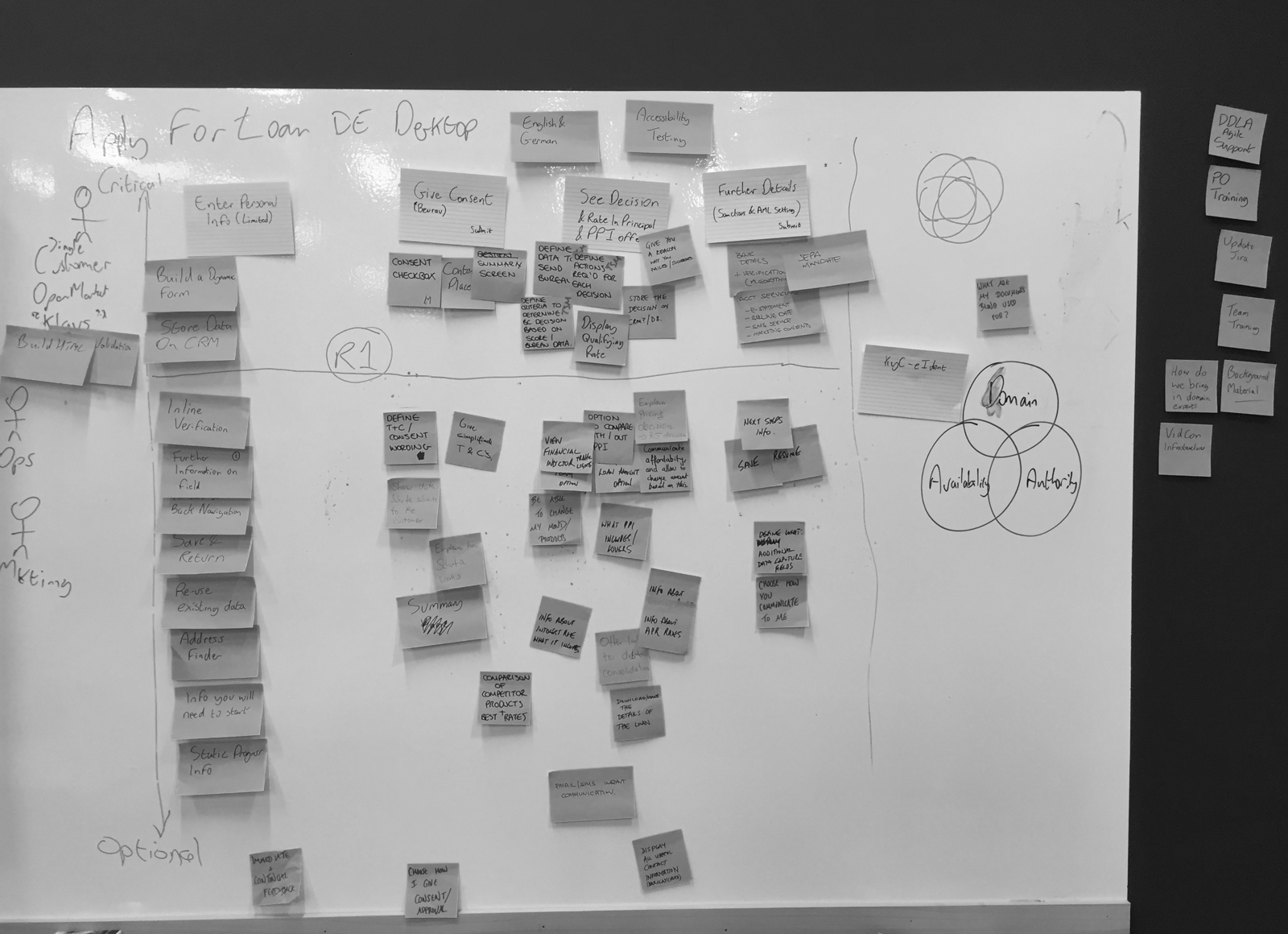

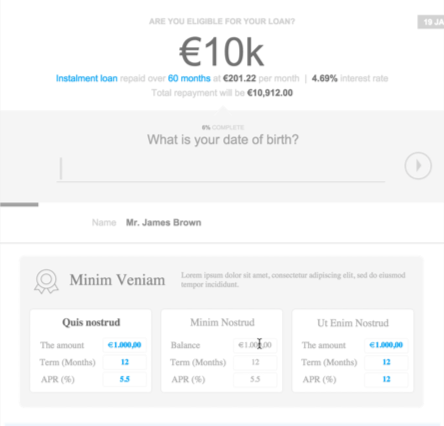

In the next few weeks to follow we worked on one week sprints and defined the customer journey down to seven interactions:

1. Calculator 2. Interest Rates 3. Application 4. PPI 5. Web ID 6. Signature 7. Completion

During our one week sprints we took a number of colleagues with varying backgrounds through the work we had conducted, asking questions and gathering feedback.

Each session involved 30 minute user tests. I conducted guerrilla user testing for two to three prototypes per week (desktop and mobile) and 30 minute think aloud sessions on filling out a loan application task based on a specific scenario where participants were asked to provide feedback while performing the task. After the user tests I would collect and analyze the feedback/pain points to improve interactions for the next build.

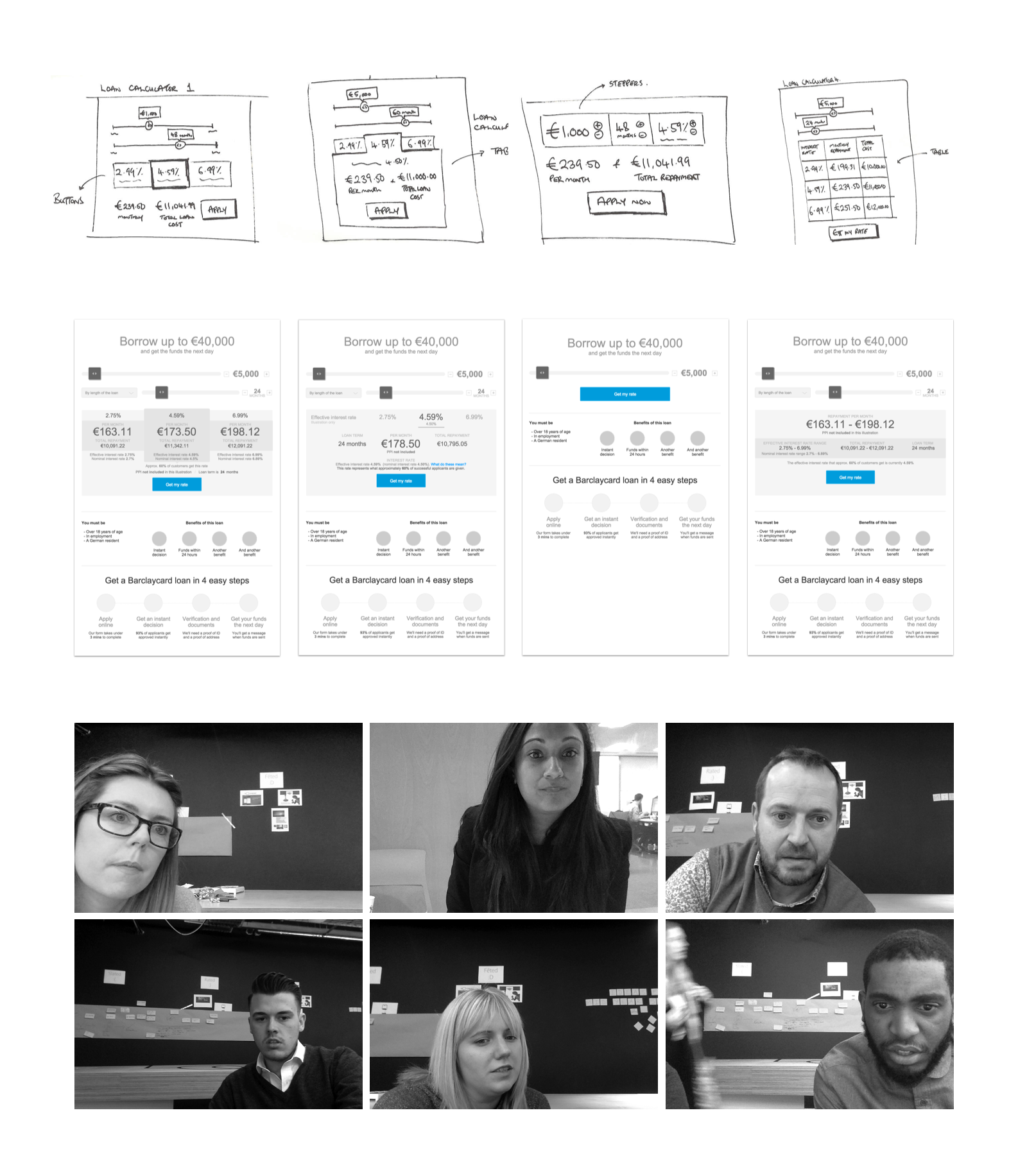

INTEREST RATES

A interesting challenge on the calculator was communicating that after the user selected their loan amount over the amount of time and clicked ‘apply’ or ‘get my rate’ for the interest rate , they would be shown three suggested interest rates, not their actual interest rate since they have not yet put in their credentials and many users thought they could select a rate out of the three options (majority of people receive a 4.59% so including 2.99% and 6.99% is just to show a range). We kept testing information that was not relevant to the user and even suggested a rate that they could not have. A solution was to ensure that the message was clear and have a link to display the range of interest rates.

PROTOTYPES

Each week I tested two to three prototypes. Since our target market was in Germany, who was going to be tested every four weeks, I was most focused on the user experience. We worked on three different experiences.

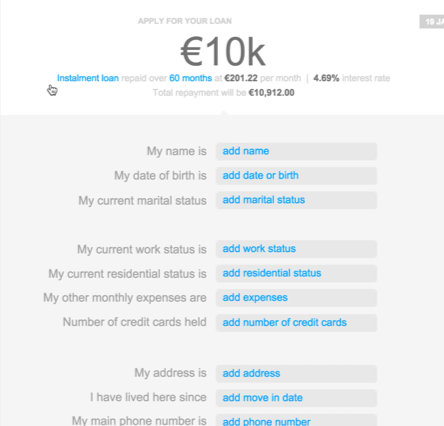

Prototype 1 approaches questions one by one as the user completes the form. Although it was perceived as striking and unusual and the user liked the idea of getting fed one question at a time, they would not have thought it was an application to apply for a loan because it does not feel 100% safe or trustworthy.

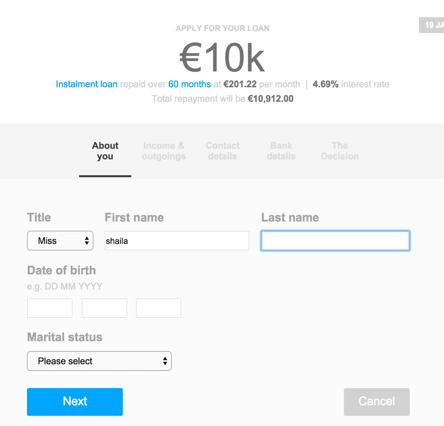

Prototype 2 approach was an in-line format that was a lean structure and had no confusion of what format to input vs. being fed single questions. Users felt that since they had to save each screen ‘save’ implies the form is going to be very long and it is simpler to just type in the box and receive a decision on the same screen.

Prototype 3 approach was the highest rated in ease of use and satisfaction. Users had a good idea of the amount of time it would take to complete because of the indications and they could see the information they entered.

THE RESULTS

Most stages of the prototype were received and highly praised by consumers and development was almost completed when my assignment ended.